Accounting for your therapy practice is where clarity either comes together or breaks down. You may be tracking income and expenses, but still not have a clear answer to what you are actually earning, how stable your cash flow is, or whether your pricing supports long-term growth.

The issue is rarely complexity. It is misalignment. When your accounting does not reflect how your practice actually earns, whether through private pay, insurance reimbursements, or programs, your financial picture becomes fragmented. That is when profitability feels unclear, tax planning becomes reactive, and financial decisions rely more on assumptions than data.

This is where accounting becomes critical. It gives you a structured view of your finances, not just for reporting, but for decisions around pricing, taxes, growth, and sustainability.

This guide breaks down accounting for therapists from a practical standpoint. You will learn how to structure your system based on your revenue model, interpret your numbers correctly, and apply accounting in real scenarios without overcomplicating your setup.

Key Takeaways

- Accounting for therapists goes beyond tracking, it provides clarity on profitability, cash flow, and overall practice performance.

- Choosing the right accounting method (cash, accrual, or hybrid) depends on how your revenue is earned and collected.

- Financial clarity comes from aligning accounting structure with your actual services and revenue streams.

- Regular expense tracking and review help maintain margins and prevent unnoticed cost increases.

- Tax planning should be ongoing, not reactive, to avoid surprises and improve financial predictability.

- Reviewing financial reports consistently enables better decisions around pricing, growth, and resource allocation.

- Strong accounting systems are built on structure and consistency, not complexity, and evolve as your practice grows.

- Simply.Coach helps therapists maintain clean, consistent operational data by centralizing sessions, client activity, programs, and progress in one place, making it easier to connect service delivery with revenue and support more accurate accounting.

What is Accounting for Therapists and Why Does it Matter for Profitability

Accounting for your therapy practice is the process of organizing, interpreting, and using your financial data to understand how your practice is actually performing. It goes beyond recording transactions.

It helps you answer questions like:

- Are you consistently profitable?

- How much of your revenue is available after expenses and taxes?

- Can your current model support growth?

At an operational level, accounting connects three things that are often treated separately, income, expenses, and timing. This becomes especially important if your practice includes a mix of private pay, insurance reimbursements, or program-based revenue, where money is earned and received at different points.

In practice, accounting shows up anywhere your financials are being evaluated, used, or questioned. This includes working with a CPA, preparing taxes, applying for loans, or making decisions about pricing and expansion. Without a structured accounting system, these moments rely on incomplete or inconsistent data.

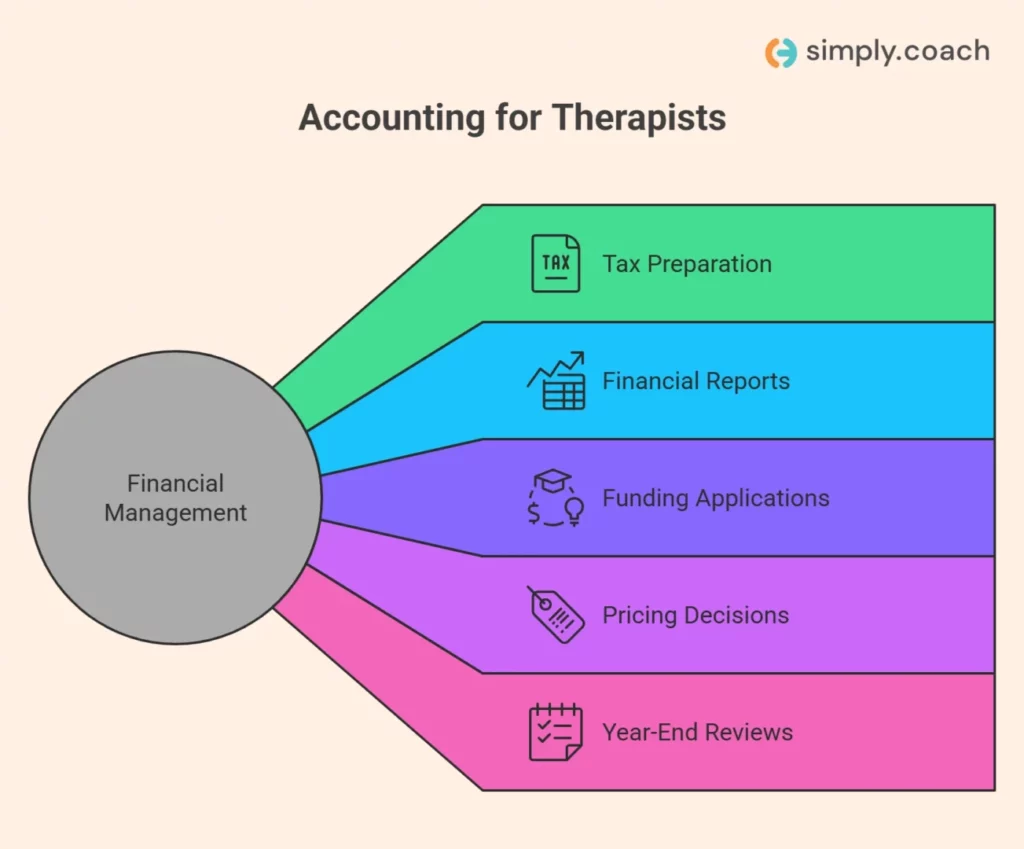

Where accounting shows up in your practice

You will see accounting influence decisions and requirements across multiple areas:

- Tax preparation and compliance: Your reported income, deductions, and liabilities depend on how accurately your financial data is structured and categorized throughout the year.

- Financial reporting (profit and loss, cash flow): These reports help you understand whether your practice is actually profitable, not just generating revenue, and whether cash flow is stable or inconsistent.

- Loan, SBA, or funding applications: Lenders evaluate your financial consistency, margins, and revenue patterns. Poorly structured accounting can delay or weaken approvals.

- Pricing and revenue decisions: Without clear visibility into costs and margins, it becomes difficult to set or adjust pricing confidently.

- Monthly or quarterly performance reviews: Accounting allows you to track trends, identify changes in income or expenses, and make adjustments before issues compound.

What accounting does not do

Accounting provides clarity, but it does not solve financial issues on its own.

- It does not increase revenue without changes to pricing, services, or demand

- It does not replace financial planning or decision-making

- It does not fix inconsistent tracking or missing data

If the underlying data is inaccurate or incomplete, the outputs will be misleading, regardless of the system you use.

Most therapy practices do not have simple income patterns. If you work with a mix of private pay, insurance, programs, or consulting, your revenue is tied to different timelines and structures.

Your accounting system needs to reflect that reality. When it does, your reports become usable, not just for compliance, but for making decisions about profitability, taxes, and growth.

Also Read: 50+ Resources, Tools, and Worksheets for Therapists

The Different Accounting Approaches Therapists Use

When it comes to accounting for therapists, there are three primary approaches: cash accounting, accrual accounting, and a hybrid model. Each one changes how your revenue, expenses, and profitability appear; so choosing the right approach is less about preference and more about how your practice actually operates.

Most therapists start with cash accounting, but as services, payment timelines, and revenue streams evolve, the limitations of a single approach become more visible.

1. Cash accounting (most common for private practice)

Cash accounting records income when money is received and expenses when they are paid. It reflects actual cash movement, which makes it easier to understand what is available in your account at any given time.

This approach works well for therapists with direct-pay models, where sessions are paid upfront or shortly after delivery. It keeps reporting simple and aligns closely with day-to-day financial reality.

However, it has limitations. It does not show money that is earned but not yet received, such as pending insurance reimbursements, which can make income appear inconsistent.

2. Accrual accounting (more complete financial view)

Accrual accounting records income when it is earned and expenses when they are incurred, regardless of when money is actually received or paid.

This creates a more accurate picture of your business over time. For example, if you complete sessions today but receive insurance payments weeks later, accrual accounting reflects that income in the period it was earned—not when it arrives.

This approach becomes more relevant in:

- Insurance-heavy practices

- Group practices with multiple revenue streams

- Situations with outstanding invoices or delayed payments

The trade-off is complexity. Accrual requires more structured tracking and reconciliation, which many solo practitioners may not need early on.

3. Hybrid approach (practical middle ground)

Many therapists operate in a hybrid model, using cash accounting for day-to-day tracking and applying accrual logic where needed.

This typically looks like:

- Tracking daily income and expenses on a cash basis

- Adjusting for unpaid income (e.g., insurance claims) during reporting

- Working with an accountant to reconcile numbers periodically

This approach provides flexibility without fully committing to accrual complexity. It is especially useful for hybrid practices that combine insurance, private pay, and program-based revenue.

The key is not to choose the most advanced system, it is to choose the one that reflects how your revenue flows and how your decisions are made.

Use cash accounting for simplicity, accrual for accuracy, and a hybrid approach when your practice sits somewhere in between.

Also Read: Top 18 Apps for Therapists to Use With Clients in 2026

Which Accounting Approach Should You Choose?

Choosing the right setup for accounting for therapists is not about what is “standard.” It is about how your practice actually earns and collects money. The same method can produce very different results depending on whether your income is immediate, delayed, or mixed across services.

A good accounting system should do two things: reflect reality and stay simple enough to maintain. The moment it stops doing either, it needs to be adjusted.

1. When cash accounting is the right fit

Cash accounting works best when your revenue is straightforward and payments are received quickly. It gives you a real-time view of what is in your account and makes day-to-day decisions easier.

This usually applies when:

- Most sessions are private pay

- Payments are collected upfront or immediately after sessions

- There are no significant receivables or delayed income

Example: A solo therapist running a private-pay practice with weekly sessions and prepaid packages. In this case, income and cash flow are closely aligned, so cash accounting provides a clear and reliable picture without added complexity.

2. When accrual accounting becomes necessary

Accrual accounting becomes relevant when there is a gap between when you earn income and when you receive it. Without it, your financials can appear inconsistent; even if your practice is stable.

This usually applies when:

- You accept insurance and deal with delayed reimbursements

- You invoice clients or organizations and receive payments later

- Your revenue timing does not match service delivery

Example: A therapist submitting insurance claims weekly but receiving payments several weeks later. Cash accounting may show fluctuating income, while accrual accounting reflects what was actually earned during that period.

3. When a hybrid approach makes more sense

Most growing practices do not fit neatly into one model. If your revenue comes from multiple sources with different payment timelines, a hybrid approach provides better balance.

This usually applies when:

- You combine insurance and private-pay clients

- You offer programs, workshops, or digital products

- Different services follow different billing structures

Example: A therapist who runs insurance-based sessions, sells coaching packages, and offers occasional group programs. Here, using cash accounting for daily tracking and applying accrual logic for delayed income creates a more accurate view without overcomplicating the system.

4. How to decide quickly (the 50% rule)

If you are unsure, use a simple rule: base your accounting method on your dominant revenue stream.

- If most income is immediate → cash accounting

- If most income is delayed → accrual accounting

- If it is mixed → hybrid, anchored to the primary source

This keeps your system aligned without trying to optimize for every edge case.

5. When it is time to change your approach

Even if your current setup works, it may not continue to as your practice evolves. The need to change usually shows up gradually.

Look for signs like:

- Income appears inconsistent despite steady client work

- You cannot clearly track what you have earned vs received

- New services do not fit your existing accounting structure

- Financial reports are no longer useful for decision-making

At that point, adjusting your accounting method is not about adding complexity; it is about restoring clarity.

The goal is not to use the most advanced system, but the one that gives you the most accurate and usable view of your practice.

In one line: Choose the accounting method that reflects how your income actually flows, then adapt it as your practice becomes more complex.

Also Read: Effective Strategies to Grow Your Therapy Practice in 2026

Accounting Tips for Therapists: Best Practices for Financial Clarity

Strong accounting for therapists is about structure, consistency, and alignment with how your practice actually operates. Most financial issues in private practice do not come from lack of effort, but from small gaps that compound over time: unclear categorization, inconsistent tracking, or systems that no longer match the business.

When the right practices are in place, accounting shifts from a reactive task to a system that supports better decisions, predictable taxes, and sustainable growth.

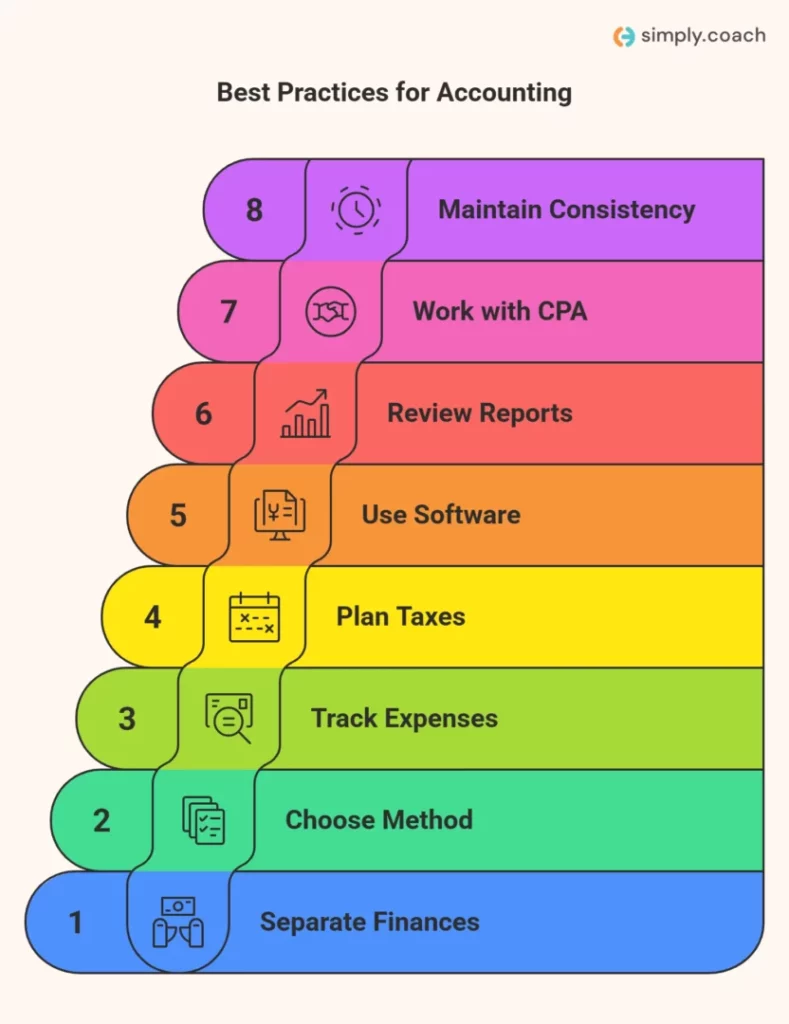

1. Separate personal and business finances early

Mixing personal and business transactions is one of the fastest ways to lose financial clarity. It introduces ambiguity into your records, makes expense categorization unreliable, and increases the chances of missed deductions or incorrect reporting.

More importantly, it limits your ability to understand how your practice is performing as a standalone business.

A structured setup should include:

- A dedicated business bank account for all income and expenses

- A separate business credit card for operational spending

- Clear boundaries between personal and practice-related transactions

This creates clean data from the start, something every other financial decision depends on.

2. Choose an accounting method that reflects your revenue timing

Your accounting method determines how your financial reality is represented on paper. If it does not match how your income flows, your reports will mislead you.

- Cash accounting reflects actual cash movement and works well for direct-pay practices

- Accrual accounting reflects earned income and becomes critical when dealing with delayed payments (like insurance)

The deeper issue is not the method itself, but misalignment. For example, using cash accounting in an insurance-heavy practice can make revenue appear inconsistent, even when the business is stable.

The goal is to ensure that your accounting method reflects:

- When revenue is earned

- When it is received

- How that timing impacts decision-making

3. Track expenses with intent and context

Expense tracking is often treated as a compliance task, but its real value is in understanding cost structure and margin.

Therapy practices typically have layered expenses:

- Fixed costs (rent, insurance, software)

- Variable costs (marketing, contractors, continuing education)

- Hidden creep (subscriptions, incremental increases, underused tools)

Without regular review, these costs grow quietly and reduce profitability.

A more effective approach includes:

- Reviewing expenses monthly or quarterly

- Identifying trends rather than just totals

- Evaluating whether each cost supports revenue or outcomes

This turns expense tracking into a tool for margin control, not just record-keeping.

4. Treat tax planning as an ongoing system

One of the biggest financial mistakes is treating taxes as a once-a-year event. In reality, taxes are directly tied to how your income evolves throughout the year.

When tax planning is reactive:

- Payments are based on outdated estimates

- Surprises are common at filing time

- Penalties or underpayments become more likely

A more structured approach includes:

- Setting aside a consistent percentage of revenue

- Adjusting estimates as income changes

- Reviewing tax position alongside financial reports

This creates predictability and removes the uncertainty that many practice owners experience around tax season.

5. Use accounting software but maintain control over structure

Accounting software can automate large parts of your workflow; transaction tracking, categorization, and reporting. But automation without structure leads to inaccurate outputs.

The risk is not in using software, but in assuming it is “correct by default.”

To make it effective:

- Set up categories that reflect your actual services and expense types

- Maintain consistency in how transactions are recorded

- Periodically audit reports for misclassification or gaps

Software should support your accounting system, not define it. The logic behind your setup matters more than the tool itself.

6. Review financial reports as decision tools, not just records

Financial reports are often generated but not actively used. This is where most of the lost value in accounting sits.

The key reports for therapists are:

- Profit and Loss (P&L): Shows whether your practice is actually profitable

- Cash flow: Shows when money enters and leaves the business

The deeper value comes from interpretation:

- Are you profitable after all expenses, not just busy?

- Are certain services driving more revenue but lower margins?

- Are expenses increasing faster than income?

Regular review (monthly or quarterly) allows you to catch patterns early and make adjustments before they impact the practice.

7. Work with a CPA who understands therapy practices

At a certain stage, accounting moves beyond tracking into strategy. This is where a CPA becomes valuable, especially one familiar with therapy practices.

Therapists often have unique financial dynamics:

- Insurance reimbursements with delayed timing

- Mixed revenue streams (therapy, programs, consulting)

- Industry-specific deductions and compliance considerations

A specialized CPA can help:

- Align your accounting structure with your business model

- Optimize tax strategy based on real income patterns

- Provide clarity on financial decisions as you grow

This reduces both risk and inefficiency.

8. Maintain consistency to prevent compounding errors

Even the best accounting systems fail without consistency. Delayed or irregular tracking introduces gaps that are difficult to correct later.

Common issues from inconsistency:

- Misclassified or missing transactions

- Inaccurate financial reports

- Increased effort during tax preparation

A consistent rhythm, weekly or monthly, ensures:

- Data stays accurate and up to date

- Reports remain reliable

- Decisions are based on current information

Consistency is what turns accounting from a cleanup task into a stable system.

When these practices are applied together, accounting becomes a source of clarity rather than confusion. You move from reacting to numbers to using them intentionally, understanding where your practice stands and where it is going.

Effective accounting is not about complexity, it is about consistent, well-structured systems that reflect how your therapy practice actually earns, spends, and grows.

Also read: Top 10 HIPAA-Compliant Therapy Practice Management Software: A 2026 Guide for Therapists

Common Accounting Mistakes Therapists Make in 2026

At an advanced level, mistakes in accounting for therapists are rarely about missing basics; they come from decisions that seem reasonable in isolation but create inconsistencies over time. As practices expand into hybrid models, these gaps start affecting tax accuracy, reporting clarity, and financial decision-making.

Below are the most common patterns, and how to correct them with a more structured approach:

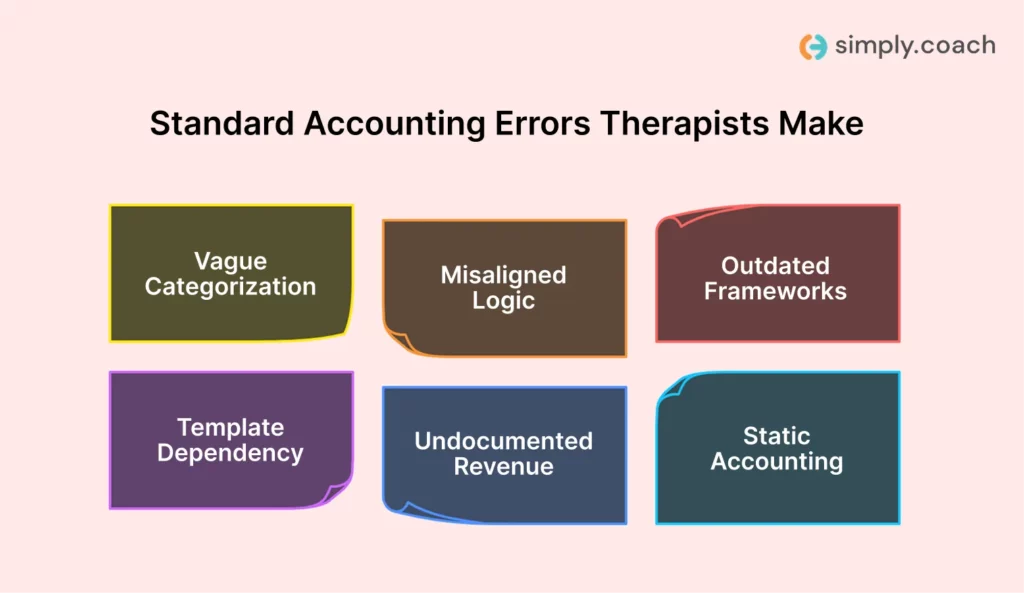

1. Choosing categories or structures because they “sound right”

Many therapists set up their accounting categories based on intuition rather than how revenue actually flows. For example, labeling everything under broad categories like “consulting” or “services” may feel convenient, but it reduces visibility.

Over time, this makes it difficult to answer key questions:

- Which services are actually driving revenue?

- Where are margins strongest or weakest?

A better approach is to structure your categories based on how your services are delivered and monetized – therapy sessions, programs, consulting, or other revenue streams – so your reports reflect reality, not assumptions.

2. Applying clinical or healthcare logic without alignment

Accounting and billing are closely linked, and mistakes often happen when clinical structures are applied without proper alignment.

This shows up when:

- Revenue is categorized as clinical without matching documentation or service type

- Financial records do not reflect how services are actually delivered

While this may not always create immediate issues, it can lead to inconsistencies in reporting, especially when working with accountants or preparing for taxes.

The fix is to ensure your accounting categories and structure align with:

- Your credentials and services

- How revenue is actually earned

- How it is billed and documented

3. Not updating accounting structure as the practice evolves

What works for a solo, session-based therapy practice often breaks when new services are introduced. Many therapists continue using the same accounting setup even after adding programs, workshops, or consulting.

This creates:

- Blended revenue categories

- Limited visibility into performance by service

- Difficulty tracking growth across different offerings

A more effective approach is to revisit your accounting structure whenever your revenue model changes. Each new service type should be reflected clearly in how income is categorized and reported.

4. Relying entirely on templates or setup platforms

Many therapists use formation services, templates, or default accounting setups to get started. While useful initially, these are often too generic to reflect a real therapy practice.

Over time, this leads to:

- Misaligned categories

- Inaccurate reports

- Limited ability to adapt as the practice grows

Instead of relying blindly on templates, treat them as a starting point. Your accounting system should evolve to match your specific services, revenue mix, and operational structure.

5. Not documenting how revenue is categorized and tracked

One of the most overlooked issues is the lack of clear documentation around accounting decisions. Categories are created, but the logic behind them is not recorded.

This becomes a problem when:

- You revisit your books months later

- You work with a CPA or bookkeeper

- You need to explain patterns during audits or reviews

Without consistency, the same type of income may be categorized differently over time.

The solution is to create a simple internal reference:

- How each service type is categorized

- How revenue is recognized (cash vs accrual logic)

- How different income streams are tracked

This ensures consistency, especially as your practice grows.

6. Treating accounting as a static setup

Many therapists approach accounting as something to “set and forget.” In reality, it is a system that needs to evolve with your business.

When it does not:

- Reports become less useful

- Financial decisions rely on incomplete data

- Tax preparation becomes more complex

A better approach is to treat accounting as a living system – reviewed periodically and adjusted as your services, revenue mix, and goals change.

When these mistakes are addressed, accounting becomes significantly more useful, not just for compliance, but for understanding and growing your practice.

In one line: Most accounting mistakes come from misalignment; fix that by structuring your system around how your practice actually earns, tracks, and evolves its revenue.

Also read: Top 9 HIPAA-Compliant Note-Taking Tools for Therapists in 2026

How Simply.Coach Helps You Maintain Clean, Consistent Data for Better Accounting

Accounting accuracy depends on what happens before the numbers. If your sessions, client activity, and delivery are not tracked consistently, your financial data becomes fragmented. That is when income feels disconnected from actual work delivered, and reports become harder to trust.

As your practice grows across private pay, insurance, programs, or consulting, this gap increases. You are no longer just tracking income, you are trying to understand what was delivered, when, and how it translates into revenue.

Simply.Coach helps bring structure to this layer. It ensures that the operational data feeding your accounting, sessions, progress, and client activity, stays consistent and organized.

Where Simply.Coach supports accounting clarity in therapy practice:

- Client workspaces (link delivery to revenue): Track sessions, notes, and client activity in one place. This helps you verify what was delivered against what was paid or expected, especially across multiple clients and services.

- Session Tracking (Reduce missed or unrecorded work): Maintain a clear record of completed, scheduled, and missed sessions. This reduces gaps between service delivery and income tracking.

- Programs and Journeys (Separate revenue streams clearly): Manage programs, packages, and structured offerings independently from 1:1 sessions. This makes it easier to align different revenue streams with your accounting categories.

- Centralized Client History (Improve consistency in reporting): Access past sessions, engagement patterns, and timelines in one place. This supports consistent categorization and reduces confusion during reporting or reviews.

- Reports and Progress Tracking (Connect outcomes with performance): Track client progress alongside service delivery. This gives additional context when evaluating which services contribute most to revenue and growth.

What this changes in your accounting system

When your operational data is structured:

- Income can be matched to actual delivery more reliably

- Different revenue streams remain clearly separated

- Reporting becomes consistent across periods

- Financial decisions are based on complete, accurate data

Simply.Coach does not replace your accounting system. It ensures the data feeding into it is structured, consistent, and aligned with how your therapy practice operates.

Also read: 20 Best Scheduling Software for Therapists in 2026: Top Picks, Features, and Pricing

Conclusion

Accounting for therapists becomes effective when it reflects how your practice actually earns, spends, and evolves. When your system aligns with your revenue model, whether private pay, insurance, or programs, your numbers become easier to interpret and act on.

Most issues do not come from complexity. They come from misalignment, inconsistent tracking, or systems that no longer match how your practice operates. Over time, this leads to unclear profitability, reactive tax planning, and limited visibility into financial performance.

A structured approach changes that. When your accounting is consistent, aligned, and regularly reviewed, it supports better decisions around pricing, expenses, and growth.

Simply.Coach, through their all-in-one HIPAA-compliant therapy practice management software, supports this by helping you maintain structured, reliable operational data, so your accounting reflects what is actually happening in your therapy practice.

FAQs

1. What is the difference between bookkeeping and accounting?

Bookkeeping focuses on recording transactions, like income and expenses, while accounting interprets that data to assess profitability, cash flow, and financial health. In practice, bookkeeping feeds the data, and accounting turns it into decisions.

2. Do therapists need to prepare financial statements regularly?

Yes, even solo therapists benefit from reviewing financial statements like profit and loss reports. Regular review helps identify trends, control expenses, and ensure the practice is financially sustainable, not just busy.

3. How often should therapists review their financials?

At a minimum, financials should be reviewed quarterly, but monthly reviews are more effective for catching issues early. Consistent review improves decision-making and prevents surprises around taxes or cash flow.

4. Is accounting different for insurance-based vs private-pay practices?

Yes, insurance-based practices often deal with delayed payments and require more structured tracking, while private-pay practices have simpler, real-time income flows. This difference affects how revenue is recognized and analyzed.

5. What are the most important expenses therapists should track?

Key expense categories include rent, software subscriptions, liability insurance, continuing education, and marketing. Tracking these consistently helps maintain control over margins and avoid unnoticed cost increases.

6. When should a therapist hire an accountant or CPA?

It becomes important when your practice grows beyond basic income tracking, especially if you have multiple revenue streams, need tax planning, or want clearer financial insights for scaling decisions.

7. Can poor accounting affect a therapist’s profitability?

Yes, poor accounting often leads to missed deductions, unclear expense tracking, and incorrect pricing decisions. Over time, this reduces profitability, even if the practice appears financially active.